A consumer price index (CPI) measures changes through time in the price level of consumer goods and services purchased by households. The CPI is defined by the United States Bureau of Labor Statistics as "a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services."[1]

The CPI is a statistical estimate constructed using the prices of a sample of representative items whose prices are collected periodically. Sub-indexes and sub-sub-indexes are computed for different categories and sub-categories of goods and services, being combined to produce the overall index with weights reflecting their shares in the total of the consumer expenditures covered by the index. It is one of several price indices calculated by most national statistical agencies. The annual percentage change in a CPI is used as a measure of inflation. A CPI can be used to index (i.e., adjust for the effect of inflation) the real value of wages, salaries, pensions, for regulating prices and for deflating monetary magnitudes to show changes in real values. In most countries, the CPI is, along with the population census and the USA National Income and Product Accounts, one of the most closely watched national economic statistics.

Introduction

Two basic types of data are needed to construct the CPI: price data and weighting data. The price data are collected for a sample of goods and services from a sample of sales outlets in a sample of locations for a sample of times. The weighting data are estimates of the shares of the different types of expenditure in the total expenditure covered by the index. These weights are usually based upon expenditure data obtained from expenditure surveys for a sample of households or upon estimates of the composition of consumption expenditure in the National Income and Product Accounts. Although some of the sampling of items for price collection is done using a sampling frame and probabilistic sampling methods, many items and outlets are chosen in a commonsense way (purposive sampling) that does not permit estimation of confidence intervals. Therefore, the sampling variance cannot be calculated. In any case, a single estimate is required in most of the purposes for which the index is used.The index is usually computed monthly, or quarterly in some countries, as a weighted average of sub-indices for different components of consumer expenditure, such as food, housing, clothing, each of which is in turn a weighted average of sub-sub-indices. At the most detailed level, the elementary aggregate level, (for example, men's shirts sold in department stores in San Francisco), detailed weighting information is unavailable, so indices are computed using an unweighted arithmetic or geometric mean of the prices of the sampled product offers. (However, the growing use of scanner data is gradually making weighting information available even at the most detailed level.) These indices compare prices each month with prices in the price-reference month. The weights used to combine them into the higher-level aggregates, and then into the overall index, relate to the estimated expenditures during a preceding whole year of the consumers covered by the index on the products within its scope in the area covered. Thus the index is a fixed-weight index, but rarely a true Laspeyres index, since the weight-reference period of a year and the price-reference period, usually a more recent single month, do not coincide. It takes time to assemble and process the information used for weighting which, in addition to household expenditure surveys, may include trade and tax data.

|

| Help end domestic violence today! |

The coverage of the index may be limited. Consumers' expenditure abroad is usually excluded; visitors' expenditure within the country may be excluded in principle if not in practice; the rural population may or may not be included; certain groups such as the very rich or the very poor may be excluded. Saving and investment are always excluded, though the prices paid for financial services provided by financial intermediaries may be included along with insurance.

The index reference period, usually called the base year, often differs both from the weight-reference period and the price reference period. This is just a matter of rescaling the whole time-series to make the value for the index reference-period equal to 100. Annually revised weights are a desirable but expensive feature of an index, for the older the weights the greater is the divergence between the current expenditure pattern and that of the weight reference-period.

Calculating the CPI for a single item

- Where 1 is usually the comparison year and CPI1 is usually an index of 100.

. The "updated cost" is the price of an item at a given year (say, the price of bread in 1982), divided by the initial year (the price of bread in 1970), multiplied by one hundred.[2]

. The "updated cost" is the price of an item at a given year (say, the price of bread in 1982), divided by the initial year (the price of bread in 1970), multiplied by one hundred.[2]Calculating the CPI for multiple items

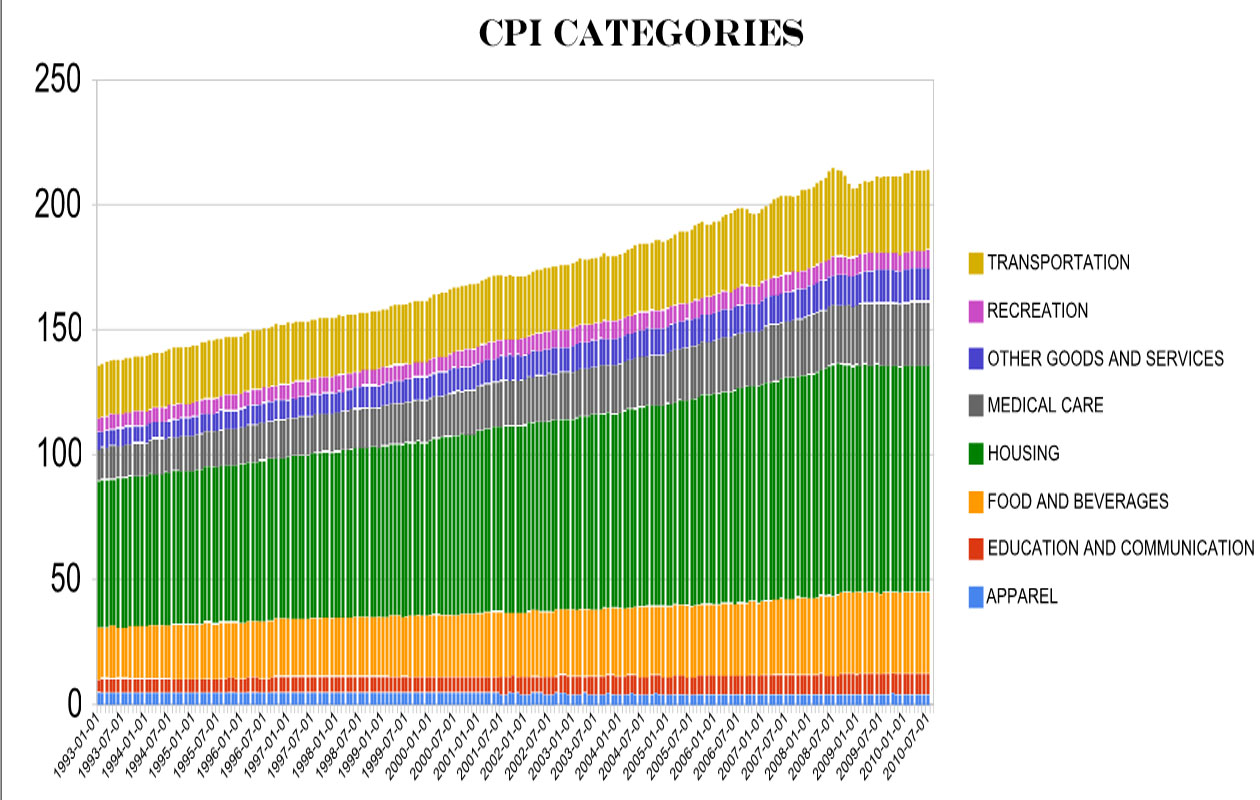

Example: The prices of 95,000 items from 22,000 stores, and 35,000 rental units are added together and averaged. They are weighted this way: Housing: 41.4%, Food and Beverage: 17.4%, Transport: 17.0%, Medical Care: 6.9%, Other: 6.9%, Apparel: 6.0%, Entertainment: 4.4%. Taxes (43%) are not included in CPI computation.[3]

Weighting

Weights and sub-indices

Weights can be expressed as fractions or ratios summing to one, as percentages summing to 100 or as per mille numbers summing to 1000.In the European Union's Harmonised Index of Consumer Prices, for example, each country computes some 80 prescribed sub-indices, their weighted average constituting the national Harmonised Index. The weights for these sub-indices will consist of the sum of the weights of a number of component lower level indices. The classification is according to use, developed in a national accounting context. This is not necessarily the kind of classification that is most appropriate for a Consumer Price Index. Grouping together of substitutes or of products whose prices tend to move in parallel might be more suitable.

For some of these lower level indexes detailed reweighing to make them be available, allowing computations where the individual price observations can all be weighted. This may be the case, for example, where all selling is in the hands of a single national organisation which makes its data available to the index compilers. For most lower level indexes, however, the weight will consist of the sum of the weights of a number of elementary aggregate indexes, each weight corresponding to its fraction of the total annual expenditure covered by the index. An 'elementary aggregate' is a lowest-level component of expenditure, one which has a weight but within which, weights of its sub-components are usually lacking. Thus, for example: Weighted averages of elementary aggregate indexes (e.g. for men’s shirts, raincoats, women’s dresses etc.) make up low level indexes (e.g. Outer garments),

Weighted averages of these in turn provide sub-indices at a higher, more aggregated level,(e.g. clothing) and weighted averages of the latter provide yet more aggregated sub-indices (e.g. Clothing and Footwear).

Some of the elementary aggregate indexes, and some of the sub-indexes can be defined simply in terms of the types of goods and/or services they cover, as in the case of such products as newspapers in some countries and postal services, which have nationally uniform prices. But where price movements do differ or might differ between regions or between outlet types, separate regional and/or outlet-type elementary aggregates are ideally required for each detailed category of goods and services, each with its own weight. An example might be an elementary aggregate for sliced bread sold in supermarkets in the Northern region.

Most elementary aggregate indexes are necessarily 'unweighted' averages for the sample of products within the sampled outlets. However in cases where it is possible to select the sample of outlets from which prices are collected so as to reflect the shares of sales to consumers of the different outlet types covered, self-weighted elementary aggregate indexes may be computed. Similarly, if the market shares of the different types of product represented by product types are known, even only approximately, the number of observed products to be priced for each of them can be made proportional to those shares.

|

| Quality unisex jewelry |

Estimating weights

The outlet and regional dimensions noted above mean that the estimation of weights involves a lot more than just the breakdown of expenditure by types of goods and services, and the number of separately weighted indexes composing the overall index depends upon two factors:- The degree of detail to which available data permit breakdown of total consumption expenditure in the weight reference-period by type of expenditure, region and outlet type.

- Whether there is reason to believe that price movements vary between these most detailed categories.

For products whose price movements can differ between regions and between different types of outlet:

- The ideal, rarely realisable in practice, would consist of estimates of expenditure for each detailed consumption category, for each type of outlet, for each region.

- At the opposite extreme, with no regional data on expenditure totals but only on population (e.g. 24% in the Northern region) and only national estimates for the shares of different outlet types for broad categories of consumption (e.g. 70% of food sold in supermarkets) the weight for sliced bread sold in supermarkets in the Northern region has to be estimated as the share of sliced bread in total consumption × 0.24 × 0.7.

The nature of the data used for weighting

No firm rules can be suggested on this issue for the simple reason that the available statistical sources differ between countries. However, all countries conduct periodical Household Expenditure surveys and all produce breakdowns of Consumption Expenditure in their National Accounts. The expenditure classifications used there may however be different. In particular:- Household Expenditure surveys do not cover the expenditures of foreign visitors, though these may be within the scope of a Consumer Price Index.

- National Accounts include imputed rents for owner-occupied dwellings which may not be within the scope of a Consumer Price Index.

The statistical sources required for regional and outlet-type breakdowns are usually weaker. Only a large-sample Household Expenditure survey can provide a regional breakdown. Regional population data are sometimes used for this purpose, but need adjustment to allow for regional differences in living standards and consumption patterns. Statistics of retail sales and market research reports can provide information for estimating outlet-type breakdowns, but the classifications they use rarely correspond to COICOP categories.

The increasingly widespread use of bar codes, scanners in shops has meant that detailed cash register printed receipts are provided by shops for an increasing share of retail purchases. This development makes possible improved Household Expenditure surveys, as Statistics Iceland has demonstrated. Survey respondents keeping a diary of their purchases need to record only the total of purchases when itemised receipts were given to them and keep these receipts in a special pocket in the diary. These receipts provide not only a detailed breakdown of purchases but also the name of the outlet. Thus response burden is markedly reduced, accuracy is increased, product description is more specific and point of purchase data are obtained, facilitating the estimation of outlet-type weights.

There are only two general principles for the estimation of weights: use all the available information and accept that rough estimates are better than no estimates.

Reweighing

Ideally, in computing an index, the weights would represent current annual expenditure patterns. In practice they necessarily reflect past expenditure patterns, using the most recent data available or, if they are not of high quality, some average of the data for more than one previous year. Some countries have used a three-year average in recognition of the fact that household survey estimates are of poor quality. In some cases some of the data sources used may not be available annually, in which case some of the weights for lower level aggregates within higher level aggregates are based on older data than the higher level weights.Infrequent reweighing saves costs for the national statistical office but delays the introduction into the index of new types of expenditure. For example, subscriptions for Internet Service entered index compilation with a considerable time lag in some countries, and account could be taken of digital camera prices between re-weightings only by including some digital cameras in the same elementary aggregate as film cameras.

Owner-occupiers and the price index

The way in which owner-occupied dwellings should be dealt with in a Consumer Price Index has been, and remains, a subject of heated controversy in many countries. The purpose of this entry is to explain why.The economists' approach

Leaving aside the quality of public services, the environment, crime and so forth, and regarding the standard of living as a function of the level and composition of individuals’ consumption, this standard depends upon the amount and range of goods and services they consume. These include the service provided by rented accommodation, which can readily be priced, and the similar services yielded by a flat or house owned by the consumer who occupies it. Its cost to a consumer is, according to the economic way of thinking, an “opportunity cost”, namely what he or she sacrifices by living in it. This cost, according to many economists, is what should form a component of a Consumer Price Index. Opportunity cost can be looked at in two ways, since there are two alternatives to continuing to live in an owner-occupied dwelling. One — supposing that it is one year’s cost that is to be considered — is to sell it, earn interest on the owner’s capital thus released, and buy it back a year later, making an allowance for its physical depreciation. This can be called the “alternative cost” approach. The other, the “rental equivalent” approach, is to let it to someone else for the year, in which case the cost is the rent that could be obtained for it. Most people do not think about their dwelling in either of these ways, but this does not bother the theoretical economist for whom consistent logic is what matters. There are, of course, practical problems in implementing either of these economists’ approaches. Thus, with the alternative cost approach, if house prices are rising fast the cost can be negative and then become sharply positive once house prices start to fall, so such an index would be very volatile. On the other hand, with the rental equivalent approach, there may be difficulty in estimating the movement of rental values of types of property which are not actually rented. If one or other of these measures of the consumption of the services of owner-occupied dwellings is included in consumption, then it must be included in income too, for income equals consumption plus saving. This means that if the movement of incomes is to be compared with the movement of the Consumer Price Index, incomes must be expressed as money income plus this imaginary consumption value. That is logical, but it may not be what users of the index want. Although the argument has been expressed in connection with owner-occupied dwellings, the logic applies equally to all durable consumer goods and services. Furniture, carpets and domestic appliances are not used up soon after purchase in the way that food is. Like dwellings, they yield a consumption service that can continue for years. Furthermore, since strict logic is to be adhered to, there are durable services as well that ought to be treated in the same way; the service consumers derive from appendectomies or crowned teeth continue for a long time. Since estimating values for these components of consumption has not been tackled, the economic theorists are torn between their desire for intellectual consistency and their recognition that inclusion of the opportunity cost of the use of durables is impracticable.Spending

Another approach is to concentrate on spending.[3] Everyone agrees that repairs and maintenance expenditure of owner-occupied dwellings should be covered in a Consumer Price Index, but the spending approach would include mortgage interest too. This turns out to be quite complicated, conceptually as well as in practice. To explain what is involved, consider a Consumer Price Index computed with reference to 2009 for just one sole consumer who bought her house in 2006, financing half of this sum by raising a mortgage. The problem is to compare how much interest such a consumer would now be paying with the interest that was paid in 2009. Since the aim is to compare like with like, that requires an estimate of how much interest would be paid now in the year 2010 on a similar house bought and 50% mortgage-financed three years ago, in 2007. It does not require an estimate of how much that identical person is paying now on the actual house she bought in 2006, even though that is what personally concerns her now. A Consumer Price Index compares how much it would cost now to do exactly what consumers did in the reference-period with what it cost then. Application of the principle thus requires that the index for our one house owner should reflect the movement of the prices of houses like hers from 2006 to 2007 and the change in interest rates. If she took out a fixed-interest rate mortgage it is the change in interest rates from 2006 to 2007 that counts; if she took out a variable interest mortgage it is the change from 2009 to 2010 that counts. Thus her current index with 1999 as reference-period will stand at more than 100 if house prices or, in the case of a fixed-interest mortgage, interest rates rose between 2006 and 2007. The application of this principle in the owner-occupied dwellings component of a Consumer Price Index is known as the “debt profile” method. It means that the current movement of the index will reflect past changes in dwelling prices and interest rates. Some people regard this as odd. Quite a few countries use the debt profile method, but in doing so most of them behave inconsistently. Consistency would require that the index should also cover the interest on consumer credit instead of the whole price paid for the products bought on credit if it covers mortgage interest payments. Products bought on credit would then be treated in the same way as owner-occupied dwellings. Variants of the debt profile method are employed or have been proposed. One example is to include down payments as well as interest. Another is to correct nominal mortgage rates for changes in dwelling prices or for changes in the rest of the Consumer Price Index to obtain a “real” rate of interest. Also, other methods may be used alongside the debt profile method. Thus several countries include a purely notional cost of depreciation as an additional index component, applying an arbitrarily estimated, or rather guessed, depreciation rate to the value of the stock of owner-occupied dwellings. Finally, one country includes both mortgage interest and purchase prices in its index.Transaction prices

The third approach simply treats the acquisition of owner-occupied dwellings in the same way as acquisitions of other durable products are treated. This means: Taking account of the transaction prices agreed;- Ignoring whether payments are delayed or are partly financed by borrowing;

- Leaving out second-hand transactions. Second-hand purchases correspond to sales by other consumers. Thus only new dwellings would be included.

Confusion

It is apparent that much of the muddle in discussing the merits of the different approaches arises from the promiscuous mixing up of arguments about feasibility, about dislike or approval of the way the index would move under a particular approach and about principles of various, often incompatible, sorts. Feasibility is naturally important. The difficulty of dealing with site values is obvious. The statisticians in a country lacking a good dwelling price index (which is required for all except the rental equivalent method) will only go along with a proposal to use such an index if they can obtain the necessary additional resources that will enable them to compile one. Even obtaining mortgage interest rate data can be a major task in a country with a multitude of mortgage lenders and many types of mortgage. Dislike of the effect upon the behaviour of the Consumer Price Index arising from the adoption of some methods can be a powerful, if sometimes unprincipled, argument. Dwelling prices are volatile and so, therefore, would be an index incorporating the current value of a dwelling price sub-index which, in some countries, would have a large weight under the third approach. Furthermore, the weight for owner-occupied dwellings could be altered considerably when reweighting was undertaken. (It could even become negative under the alternative cost approach if weights were estimated for a year during which house prices had been rising steeply). Then there is the point that a rise in interest rates designed to halt inflation could paradoxically make inflation appear higher if current interest rates showed up in the index. The economists’ principles are not acceptable to all; nor is insistence upon consistency between the treatment of owner-occupied dwellings and other durables.Clarity

Much would be gained if two sets of problems were distinguished.*- What is the Consumer Price Index to measure?

- How can that be achieved?

- What is the question that should be answered? This is a matter for policy makers and other users of the Consumer Price Index.

- How can it best be answered? This is a matter for the statisticians.#

- Opportunity cost. What is the change through time in what would be the opportunity cost of the reference-period consumption of the services of owner-occupied dwellings?

- Spending. What is the change through time in the cash outlays that would correspond to the reference-period cash outlays in respect of owner-occupied dwellings?

- Transactions. What is the change through time in what would be the purchase value of the reference-period net acquisition of owner-occupied dwellings by consumers?

History

Between 1971 and 1977, the United States CPI increased 47%.[4]In 2009, the Consumer Price Index fell for the first time since 1955.[5]

See also

- Consumer price index by country

- Core inflation

- Cost of living index

- FRED (Federal Reserve Economic Data)

- Harmonised Index of Consumer Prices (HICP)

- Hedonic regression

- Higher Education Price Index

- Household final consumption expenditure (HFCE)

- GDP deflator

- Inflation adjustment

- Inflation rate

- List of economics topics

- Market basket (basket of goods)

- Personal consumption expenditures price index (PCEPI)

- Producer Price Index (PPI)

- Quality bias

- RPIX

- Substitution

- World inflation crisis

References

| This article includes a list of references, but its sources remain unclear because it has insufficient inline citations. Please help to improve this article by introducing more precise citations where appropriate. (October 2008) |

| This article needs additional citations for verification. Please help improve this article by adding reliable references. Unsourced material may be challenged and removed. (January 2009) |

- ^ "Consumer Price Index - Frequently Asked Questions (FAQs)". Bureau of Labor Statistics. Accessed September 10, 2010. http://www.bls.gov/cpi/cpifaq.htm.

- ^ Education 2020 Homeschool Console, subject Economics, lecture "Inflation". Formula described within.

- ^ Bloomberg Business News, Social Security Administration

- ^ Frum, David (2000). How We Got Here: The '70s. New York, New York: Basic Books. p. 324. ISBN 0465041957.

- ^ Harper's Magazine http://harpers.org/archive/2009/04/WeeklyReview2009-04-21

External links

- ILO CPI manual This large manual produced co-operatively by a number of international organizations is the standard work on the methods of compiling consumer price indexes and on the underlying economic and statistical theory.

- myCPI.info Project for establishing alternative CPI data based on users inputting and tracking their personal CPI.

- "The Consumer Price Index and index number purpose": A technical article by economist W.E. Diewert

- [1] Bureau of Labor Statistics - Consumer Price Index (CPI)

- Specific countries

- International:

- Australia:Australian CPI

- France:

- Canada; [2]

- Germany:[3], Federal Statistical Office of Germany

- Hong Kong: Hong Kong Consumer Price Index (CPI) - Census and Statistics Department

- Italy: Indici dei prezzi al consumo, ISTAT

- Spain: [4], Instituto Nacional de Estadística

- New Zealand: [5] from Statistics New Zealand

- Norway;

- Sweden:

- Denmark:

- United Kingdom:

- United States:

- Consumer Price Index Home Page, U.S. Department of Labor, Bureau of Labor Statistics

- A detailed account of the US index

- Inflation Calculator

- Historical US CPI chart, monthly data since 1947

- CPI categories 1993-2010

- Alternate non official CPI measures

- An inflation research site and personal inflation rate calculator

{kind=link}